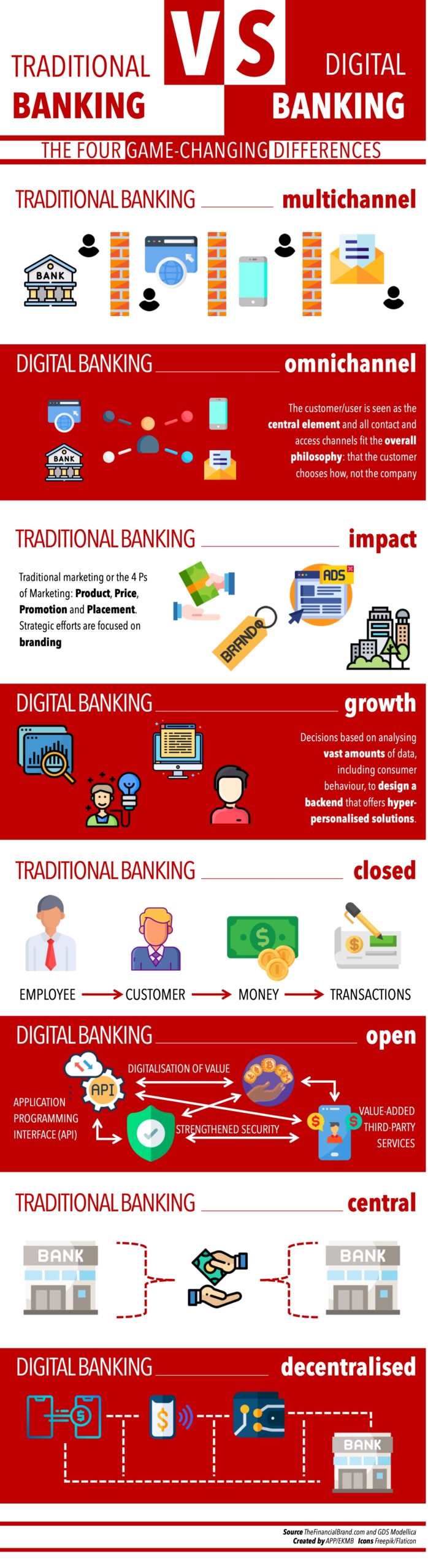

A Comprehensive and Holistic Approach to Digital Banking to Get Closer to the Customer

A Comprehensive and Holistic Approach to Digital Banking to Get Closer to the Customer Press

The customer lifecycle in a digital environment

The customer lifecycle in a digital environment Press ReleaseMadrid, 11th May 2021The digital customer lifecycle

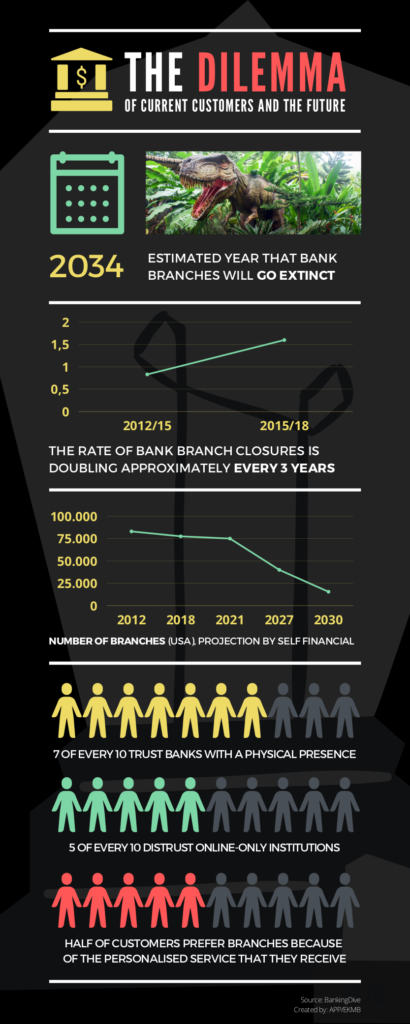

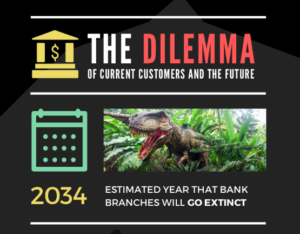

The dilemma for the banking industry: current customers and the future

The dilemma for the banking industry: current customers and the future GDS Modellica The banking